The Atal Pension Yojana Scheme (APY Scheme) is government-backed in India aimed at providing financial security to citizens of the unorganized sector after the age of 60. In 2015, Prime Minister Narendra Modi initiated the launch.

Atal Pension Yojana Scheme (APY) is a social security scheme launched by the Government of India in 2015. The primary objective of this scheme is to provide a sustainable pension to the unorganized sector workers who are not covered by any formal pension scheme. This is named in honor of Atal Bihari Vajpayee, a former Prime Minister of India.

There are so many benefits to avail of APY such as it provides guaranteed minimum pension, government co-contribution, tax benefits, flexibility in contributions, etc.

Here is the Atal Pension Yojana Chart which shows how much pension you will get at what entry age, and how many years you have to contribute.

|

Entry Age (Years) |

Total years of contribution |

The monthly contribution amount required |

||||

|

Monthly pension Rs. 1000 |

Monthly pension Rs. 2000 |

Monthly pension Rs. 3000 |

Monthly pension Rs. 4000 |

Monthly pension Rs. 5000 |

||

|

18 |

42 |

Rs. 42 |

Rs. 84 |

Rs. 126 |

Rs. 168 |

Rs. 210 |

|

19 |

41 |

Rs. 46 |

Rs. 92 |

Rs. 138 |

Rs. 183 |

Rs. 228 |

|

29 |

40 |

Rs. 50 |

Rs. 100 |

Rs. 150 |

Rs. 198 |

Rs. 248 |

|

21 |

39 |

Rs. 54 |

Rs. 108 |

Rs. 162 |

Rs. 215 |

Rs. 269 |

|

22 |

38 |

Rs. 59 |

Rs. 117 |

Rs. 177 |

Rs. 234 |

Rs. 292 |

|

23 |

37 |

Rs. 64 |

Rs. 127 |

Rs. 192 |

Rs. 254 |

Rs. 318 |

|

24 |

36 |

Rs. 70 |

Rs. 139 |

Rs. 208 |

Rs. 277 |

Rs. 346 |

|

25 |

35 |

Rs. 76 |

Rs. 151 |

Rs. 226 |

Rs. 301 |

Rs. 376 |

|

26 |

34 |

Rs. 82 |

Rs. 164 |

Rs. 246 |

Rs. 327 |

Rs. 409 |

|

27 |

33 |

Rs. 90 |

Rs. 178 |

Rs. 268 |

Rs. 356 |

Rs. 446 |

|

28 |

32 |

Rs. 97 |

Rs. 194 |

Rs. 292 |

Rs. 388 |

Rs. 485 |

|

29 |

31 |

Rs. 106 |

Rs. 212 |

Rs. 318 |

Rs. 423 |

Rs. 529 |

|

30 |

30 |

Rs. 116 |

Rs. 231 |

Rs. 347 |

Rs. 462 |

Rs. 577 |

|

31 |

29 |

Rs. 126 |

Rs. 252 |

Rs. 379 |

Rs. 504 |

Rs. 630 |

|

32 |

28 |

Rs. 138 |

Rs. 276 |

Rs. 414 |

Rs. 551 |

Rs. 689 |

|

33 |

27 |

Rs. 151 |

Rs. 302 |

Rs. 453 |

Rs. 602 |

Rs. 752 |

|

34 |

26 |

Rs. 165 |

Rs. 330 |

Rs. 495 |

Rs. 659 |

Rs. 824 |

|

35 |

26 |

Rs. 181 |

Rs. 362 |

Rs. 543 |

Rs. 722 |

Rs. 902 |

|

36 |

24 |

Rs. 198 |

Rs. 396 |

Rs. 594 |

Rs. 792 |

Rs. 990 |

|

37 |

23 |

Rs. 218 |

Rs. 436 |

Rs. 654 |

Rs. 870 |

Rs. 1087 |

|

38 |

22 |

Rs. 240 |

Rs. 480 |

Rs. 720 |

Rs. 957 |

Rs. 1196 |

|

39 |

21 |

Rs. 264 |

Rs. 528 |

Rs. 792 |

Rs. 1054 |

Rs. 1318 |

|

40 |

20 |

Rs. 291 |

Rs. 582 |

Rs. 873 |

Rs. 1164 |

Rs. 1454 |

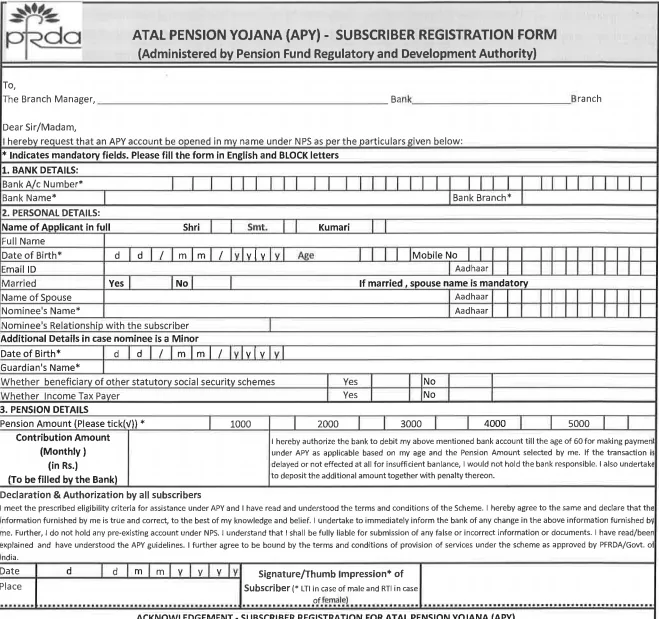

To open an Atal Pension Yojana Scheme (APY) account, you can follow these steps to open the account seamlessly.

Step 1: Go to the nearest bank branch and get the “Atal Pension Yojana Registration Form” or download it from here.

Step 2: Complete the registration form with accurate and up-to-date information. Provide details such as your name, address, age, nominee details, Aadhaar number, bank account number, and mobile number.

Step 3: Submit the filled-in registration form along with any supporting documents, such as a copy of Aadhaar card, to the bank officials.

Step 4: Select the pension amount you wish to receive and the contribution period based on your age and financial capacity, and provide authorization for auto-debit from your bank account.

Step 5: Your first contribution amount will be deducted from your linked bank account at the time of account opening. The bank will provide you with a receipt number or PRAN (Permanent Retirement Account Number).

Step 6: After the account is opened, you will receive a PRAN card (Permanent Retirement Account Number) from the National Pension System (NPS) Central Recordkeeping Agency (CRA). This card will have your unique PRAN, and it is essential for tracking your contributions and pension details.

The Atal Pension Yojana (APY) is a social security program supported by the government of India, created to offer a consistent monthly pension to individuals working in the informal sector.

Here are the eligibility criteria:

There are several charges associated with maintaining an APY account, categorized into two types: one-time charges and recurring charges.

There are some tax benefits to avail of the Atal Pension Yojana Scheme such as the Deduction under Section 80CCD(1B), Section 80CCD(1), etc.

Deduction under Section 80CCD(1B): You can claim a deduction of up to 10% of your gross total income or Rs. 1.5 lakh per year, whichever is lower, for contributions made to your APY account. This deduction falls under the same section as Tier 1 NPS contributions.

Additional deduction for low-income earners: Under Section 80CCD(1), an additional deduction of up to Rs. 50,000 per year is available for individuals with a gross total income below Rs. 10 lakh. However, this deduction cannot be claimed in addition to the 10% deduction mentioned above.

Partial tax exemption: Up to 40% of the lump sum received at the time of exit from the scheme after attaining the age of 60 is exempt from income tax.

Annuity taxation: The monthly pension received after maturity is taxed as per your applicable income tax slab.

Here are the penalties for late payments of APY Scheme that you should look at in 2024:

|

Monthly Contribution Range |

Penalty for Late Payment |

|---|---|

|

Up to Rs. 100 |

Rs. 1 per month |

|

Rs. 101 to Rs. 500 |

Rs. 2 per month |

|

Rs. 501 to Rs. 1,000 |

Rs. 5 per month |

|

More than Rs. 1,000 |

Rs. 10 per month |

Currently, there is no centralized toll-free helpline number for Atal Pension Yojana. APY accounts can be opened in different banks across India. Therefore, for any issues related to your APY account, you should contact the bank where you have opened your pension account. However, for APY assistance, you can reach out to the following toll-free numbers:

Customer Support Toll-Free Numbers:

CRA (Central Recordkeeping Agency): 1800-222-080

NPS Helpdesk: 1800-110-708

Read More:

Aam Aadmi Bima Yojana (AABY) - Application, & Benefits

Senior Citizen Saving Scheme (SCSS) - Interest Rate 2024

Best Monthly Income Scheme in India 2024

Pradhan Mantri Vaya Vandana Yojana Scheme (PMVVY)

Sukanya Samriddhi Yojana - Interest Rate 2024

In conclusion, the Atal Pension Yojana is an initiative by the Indian government to promote financial security for the elderly population. By providing a guaranteed pension to those who have contributed during their working years, the scheme aims to alleviate poverty and ensure a comfortable retirement for all citizens. The scheme's low entry age and affordable contributions make it accessible to a wide range of individuals, particularly those in the unorganized sector.

Life Insurance

Life Insurance Health Insurance

Health Insurance Pet Insurance

Pet Insurance Motor Insurance

Motor Insurance Travel Insurance

Travel Insurance Commercial Insurance

Commercial Insurance